- Profit Pulse

- Posts

- 🎬 Netflix Q4 2025 Earnings Breakdown

🎬 Netflix Q4 2025 Earnings Breakdown

Streaming Giant or Cash-Flow Machine?

Henry Dalsania

February 12, 2026

On January 20, 2026, Netflix presented their 2025 Q4 earnings. Shedding light on the quarter as well as the full year, Netflix showed why it's still the king of streaming. Let’s be honest — most earnings breakdowns are either

dry accounting lectures… or

hype pieces disguised as analysis.

This isn’t that.

We’re breaking Netflix down through the Profit Pulse lens — what actually matters for long-term investors who want conviction, not dopamine hits.

And yes… there are some big strategic moves under the surface that Wall Street headlines barely scratched. In fact, the earnings were overshadowed by the pending Warner Bros/Discovery deal.

So let’s dig in.

📊 The Big Picture — Strong Quarter, Stronger Narrative

🔢 Key Numbers (Q4 2025)

Revenue: $12.05B (+18% YoY)

Operating Income: ~ $3.0B (+30% YoY)

Operating Margin: ~25% (+2 pts YoY)

EPS: $0.56 vs $0.43 (+31% YoY)

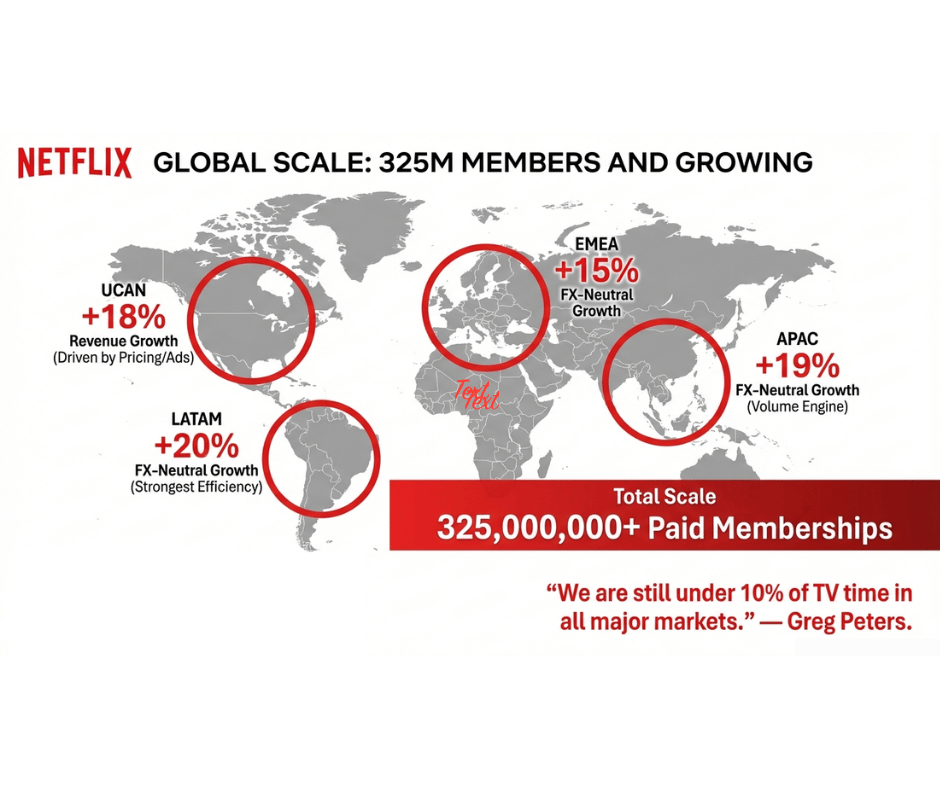

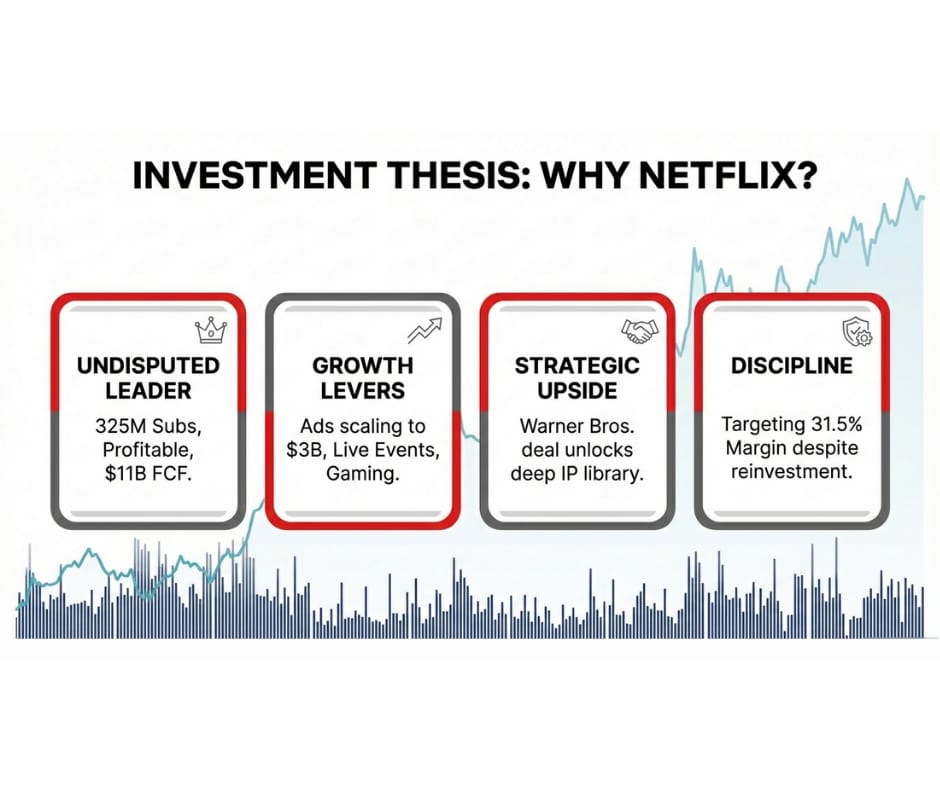

Paid memberships crossed 325M globally

📉 Compared to Previous Quarter (Q3 2025)

Revenue rose from $11.51B → $12.05B

Operating margin dropped from 28.2% → 24.5% due to content timing

👉 Translation:

Margins dipped because Netflix intentionally leaned into heavier content spending, product launches, and growth investments designed to drive future subscribers and ad revenue. This wasn’t a sign of weakening demand or operational cracks — it was a calculated reinvestment phase aimed at strengthening the long‑term engine.

🧠 Profit Pulse Takeaway

Revenue growth paired with year-over-year margin expansion is a classic signal of real operating leverage — the kind that comes from a business scaling efficiently, not from financial engineering or short-term tricks. When a company continues to grow revenue while improving profitability over time, it shows that the underlying model is strengthening and monetization is improving. Yes, margins dipped sequentially this quarter, but zoom out: the broader trajectory remains healthy because Netflix is still compounding revenue and investing behind future growth drivers.

In true Profit Pulse fashion, temporary margin compression during heavy investment cycles shouldn’t rattle long-term investors. As long as revenue keeps compounding and strategic spending is building future cash flow engines, these short-term dips are often the setup for the next leg of earnings growth.

Or in plain English:

Netflix didn’t suddenly forget how to run a business — it deliberately spent more today to build a bigger, more profitable machine tomorrow.

💰 Advertising — The Silent Growth Monster

This is likely THE most underappreciated part of Netflix’s story.

📊 The Numbers

Ad revenue: > $1.5B in 2025

Up 2.5x YoY

Ad tier users: 190M MAU

50% of new signups choose ad tier in some markets

Management expects:

👉 Ad revenue roughly doubling in 2026

🧠 What This Means

Netflix is becoming:

Subscription business – still the core engine, but now with pricing power, tiered offerings, and global scale that drive predictable recurring revenue and long‑term cash flow visibility.

Advertising platform – a rapidly growing, high‑margin layer on top of the subscription model that monetizes engagement without relying solely on price increases.

Data-driven media company – leveraging viewing data, engagement trends, and personalization algorithms to decide what gets produced, promoted, and monetized more efficiently than traditional studios.

This is a structural shift in how Netflix makes money and compounds value. It’s no longer just competing on shows alone — it’s building a multi‑layered monetization machine designed to extract more revenue from the same viewer base over time.

Not just “the company that made Stranger Things.”

🎯 Profit Pulse Insight

Advertising = high-margin incremental revenue.

Once infrastructure is built, ad dollars drop into operating income faster than subscription growth alone.

That’s why operating margins keep expanding long term.

🎥 Content Strategy — Fandom > Hours Watched

Key titles driving engagement:

Stranger Things Final Season — 120M views

Frankenstein — 102M views

Squid Game 2 drove subscriber growth

Management emphasis: “Fandom is such a powerful engine… creates advocates.”

🧠 Translation

They’re not chasing content volume anymore — they’re reallocating capital toward fewer, bigger, more defensible content bets that can compound value over time.

They’re deliberately building IP ecosystems designed to extend beyond a single season or viral moment and into long‑term monetization engines.

Think:

franchises – repeatable story universes that drive sequels, spin‑offs, global releases, and consistent engagement across years, not weeks.

merchandising – turning popular characters and shows into physical products, licensing deals, and additional revenue streams that go far beyond subscription fees.

long-term brand loyalty – creating fan communities and cultural moments that reduce churn, increase pricing power, and keep viewers emotionally invested in the platform.

Basically… Disney’s playbook — but executed faster, powered by data, and scaled globally from day one.Not just “the company that made Stranger Things.”

🎯 Profit Pulse Insight

Strong IP = pricing power + retention + recurring engagement.

That’s what turns content spending into durable moats.

📡 Live Events, Gaming & New Growth Engines

Netflix is quietly morphing into an entertainment platform — not just streaming.

🚀 Growth Initiatives

WWE Raw starting 2026

MLB events + global sports streaming

Cloud gaming rollout to one-third of members

Video podcasts launching with major partners

🧠 Why This Matters

Every new format:

increases time spent

diversifies revenue

expands ad inventory

And remember:

Netflix still has less than 10% of total TV time in major markets.

That means runway… not saturation.

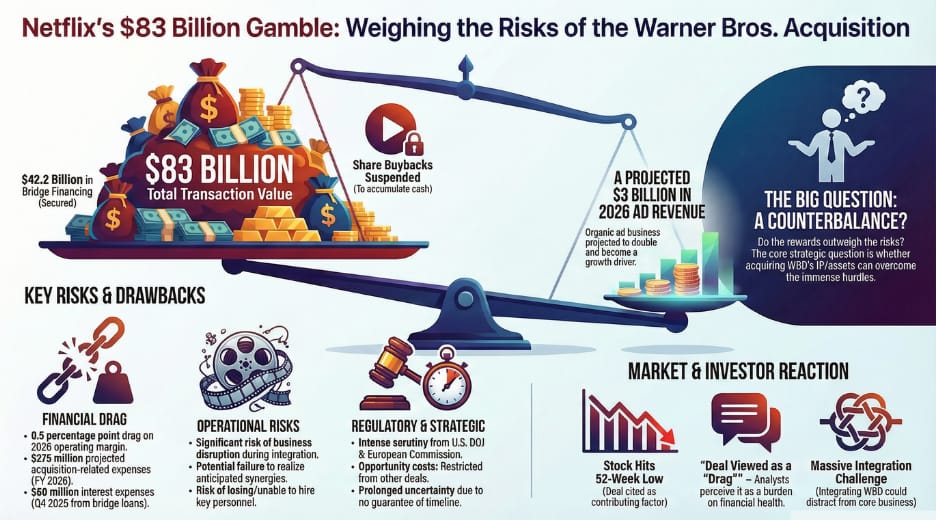

🧾 The Strategic Bombshell — Warner Bros Discovery Deal

Netflix is acquiring WBD in an all-cash transaction funded through a combination of existing cash reserves, strong ongoing free cash flow generation, and balance‑sheet financing capacity — a structure that signals management’s confidence in future cash flows while avoiding shareholder dilution.

Implied acquisition price of $27.75 per share — a premium valuation that reflects the strategic value of WBD’s IP library, premium content portfolio, and long‑term revenue synergies Netflix expects to unlock through scale and integration.

Strategic benefits:

HBO prestige content

Massive IP library

theatrical distribution network

🧠 Profit Pulse Interpretation

This is not just a merger — and it hasn’t been without criticism. Skeptics worry the integration could pressure near‑term operating margins as Netflix absorbs legacy studio costs, restructures overlapping operations, and ramps investment to fully monetize WBD’s content library. Others question whether cultural differences between a tech‑driven streamer and a traditional media conglomerate could slow execution or dilute Netflix’s historically lean operating model. Management’s response has been clear: short‑term margin compression is expected, but they believe scale synergies, advertising expansion, and deeper IP monetization will ultimately expand margins and strengthen long‑term cash flow.

Business evolution: transitioning from a pure streaming company → a full-stack entertainment platform

Market debate: Wall Street remains split on integration risk, margin pressure, and execution complexity

Key investor question: does this acquisition deepen Netflix’s competitive moat and long-term pricing power?

Profit Pulse view: yes — deeper IP, broader distribution, and layered monetization strengthen the long-term model

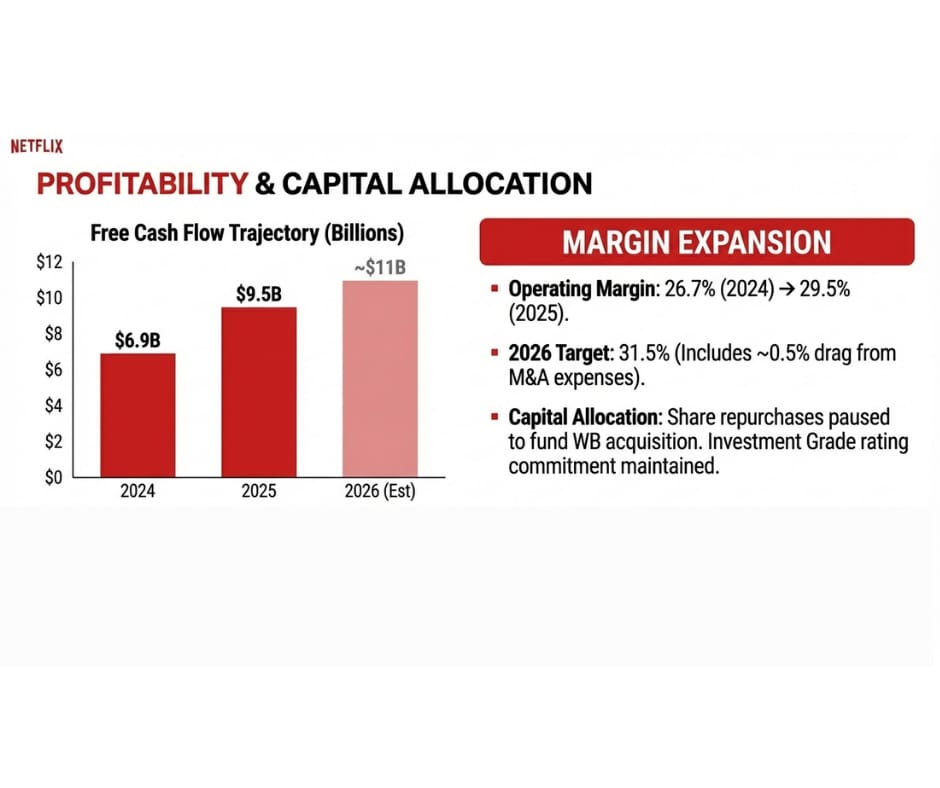

🔮 2026 Guidance — Still a Growth Story

Netflix expects:

Revenue: $50.7B–$51.7B

Operating margin: 31.5%

Free cash flow ≈ $11B

Key drivers:

Ads scaling

Pricing increases

Membership growth

📌 What This Means for Long-Term Investors

Netflix is evolving into:

Subscription platform – a global recurring revenue engine with increasing pricing power, tiered offerings, and expanding monetization per user rather than relying solely on raw subscriber growth.

Advertising powerhouse – layering a high‑margin ad business on top of its massive engagement base, creating a second profit engine that scales faster than traditional subscription revenue alone.

Live sports distributor – using marquee events and real‑time content to increase engagement hours, attract new demographics, and unlock premium advertising inventory.

Gaming ecosystem – building interactive entertainment layers that deepen user stickiness, extend IP into new formats, and increase lifetime customer value beyond passive viewing.

Premium IP conglomerate – consolidating franchises, licensed content, and proprietary universes into a diversified entertainment portfolio designed for long‑term monetization across streaming, merchandise, live events, and future media formats.

🎯 Bottom Line

Netflix isn’t just growing subscribers anymore.

It’s stacking:

multiple revenue streams

premium IP

advertising leverage

global scale

And the most important takeaway?

👉 The business model is getting stronger… while profitability improves.

NFLX

Breakdown of the results. More information. Better decisions.

Henry

Profit Pulse